What will be discussed:

Pag-IBIG Funds

· Steps to avail a Housing loan thru Pag-IBIG

· How much can I borrow against my monthly income

Government Service Insurance System (GSIS)

· GSIS Conso-Loans and steps on how to avail of it

· What is the difference between a regular loan and a Conso-Loan?

· GSIS eCard Plus and steps on how to avail of it

Social Security System (SSS)

· Loans through SSS and how to Avail of it

What is a Government loan?

A Government loan is a loan that is provided by the government of the country which you are a citizen. This usually needs membership by the borrower and can be done by filling up a form at the government office or, if you are employed in the Philippines, your company will be the one to register you with the government office. Monthly contributions will be deducted from your salary and will be forwarded to the government agency and serve as savings and to be a basis for loaning in the future (if the payments are regular)

Government Loan Provider in the Philippines

Pag-IBIG Fund

About Pag-IBIG Fund

Pag-IBIG Funds is a government institution that seeks to provide a national savings program and affordable shelter financing for Filipino workers. Pag-IBIG stands for “Pangtutulungan (Cooperation) sa Kinabukasan (for the future): Ikaw (You), Bangko (the Bank) at Gobyerno (and the Government)“

Under the Republic Act No. 9679, also known as the Home Development Fund Law of 2009, Pag-IBIG membership id mandatory for all employees covered by the Social Security System (SSS) and for all employees covered by the Government Service Insurance System (GSIS) as well as uniformed members of the Armed Forces of the Philippines (AFP), Bureau of Fire Protection (BFP), Bureau of Jail Management and Penology (BJMP), the Philippine National Police (PNP), overseas Filipino workers, and Filipinos employed by foreign employers, deployed locally or abroad.

The law also grants Tax payment exemption to employees with a monthly compensation of P1,500 and below, the contribution amounts to 1%percent of their income plus 2% covered by the employer. For employees above P1,500, contribution amounts to 2% of their income plus 2% covered by their employer. These contributions are deducted from the gross income before the computation of income tax.

A member may withdraw his savings after accumulating 20 years (equivalent to 240 months) of membership in the fund.

Circumstances such as retirement, permanent departure of the country or permanent or total disability also allows a member to withdraw his savings regardless of how much the savings sum up to.

Loans through Pag-IBIG

Pag-IBIG also offers short-term loans to members who have made at least 24 monthly contributions. Housing loans are available to members under its end-user financial program. Eligible member are those with at least 24 monthly contributions (but not more than 65year old at the time of application), and those who will pass satisfactory background checks by the developer and Pag-IBIG fund. (Members availing this loan must have the capacity to acquire real property, no outstanding Pag-IBIG housing loan and does not have a previous Pag-IBIG loan foreclosed or canceled.

Steps to avail a Housing loan thru Pag-IBIG

1. Attend a loan counseling session at the Pag-IBIG office and accomplish a Preliminary Loan Counseling Questionnaire, Housing Loan Application (HLA) and Membership Status Verification Slip (MSVS). If you are eligiblefor the loan, then secure the Checklist of Requirements (COR) ( the requirements would depend on the loan purpose).

2. Submit HLA with complete requirements, and pay the processing fee of P1,000 (non-refundable).

3. Receive Notice of Loan Approval/Letter of Guaranty and sign loan documents.

4. Proceed to the following:

· Bureau of Internal Revenue for payment of documentary stamps and capital gains tax

· Registry of Deeds for transfer of the title and annotation of mortgage

5. Submit the following documents to Pag-IBIG for the release of loan proceeds:

• Original Transfer Certificate of Title (TCT) in the name of the applicant with annotated mortgage

• DOAS with original RD stamp

• New Tax Declaration in the name of the applicant

• Updated Real Estate Tax Receipt (for house and lot, if applicable)

• Occupancy Permit (secured from LGU Engineering Office, if applicable)

• Assignment of Loan Proceeds

6. Pay the first monthly amortization on the month immediately following the loan take-out/final loan release.

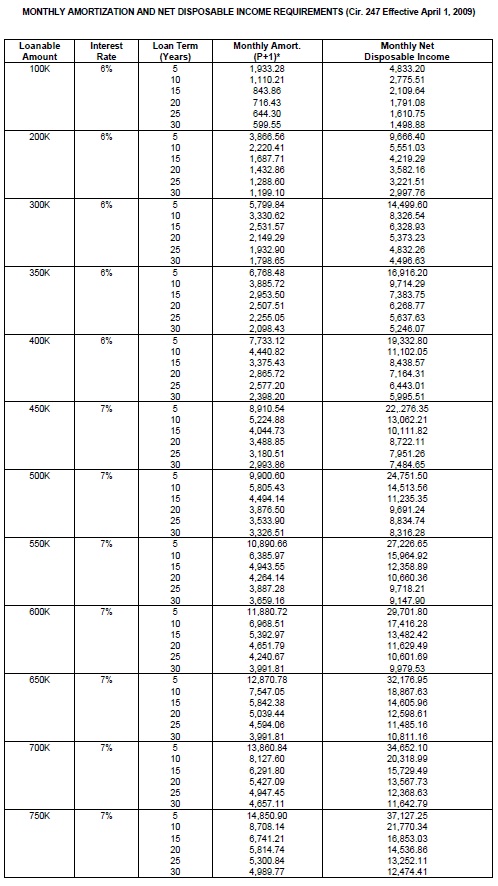

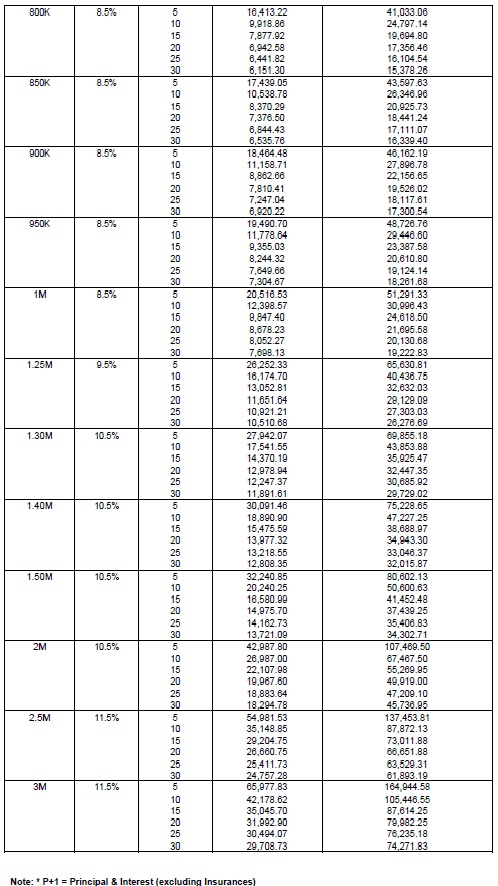

How much can I borrow against my monthly income

Before you put any down payment to any property, and think of getting the loan from Pag-ibig Fund, please be aware that mainly, your loan entitlement will be assessed against your Disposable Income.

This table may vary in time, but can be used as a basis on how much you can borrow with your current income:

See Pag-IBIG loans application forms here: http://www.pagibigfund.gov.ph/dlforms.aspx

Any further inquiries about Pag-IBIG?

Government Service Insurance System (GSIS)

About GSIS

The Government Service Insurance System or GSIS (Filipino: Paseguruhan ng mga Naglilingkod sa Pamahalaan) is a government owned and controlled corporation (GOCC) of the Philippines. Created by Commonwealth Act No. 186 passed on November 14, 1936, the GSIS provides and administers the following social security benefits for government employees: compulsory life insurance, optional life insurance, retirement benefits, disability benefits for work-related risks and death benefits. In addition, the GSIS is entrusted with the administration of the General Insurance Fund by virtue of RA656 of the Property Insurance Law. It provides insurance coverage to assets and properties which have government insurable interests.

Coverage

The GSIS covers all government workers regardless of their employment status, except employees who have separate retirement schemes under special laws, including, members of the Judiciary and Constitutional Commissions, contractual employees who have no employee-employer relationship with their agencies, uniformed members of the Armed Forces of the Philippines, and the Philippine National Police, including the Bureau of Jail Management and Penology, and the Bureau of Fire Protection.

Benefits and Services

MEMBERS and pensioners of the Government Service Insurance System can now apply for a housing loan through the Home Development Mutual Fund or Pag-Ibig. The principal benefit package of the GSIS consists of compulsory and optional life insurance, retirement, separation and employee's compensation.

Active GSIS members are entitled to the following loan privileges: salary, policy, emergency and housing loans (through Pag-IBIG).

See GSIS application form here http://www.gsis.gov.ph/downloads/Consoloan_Application-REV%20120111.pdf

Conso -Loans

Regular loans aren’t the only services the GSIS provides to their members. They have a product called Conso-Loans which helps members restore their status as a member and lower their amortization, especially if they are experiencing difficulty in paying their loans and have incurred arrears, penalties, and surcharges. Although this benefit can only be applied within the first availment of the Conso-Loan

What is a GSIS Conso-Loans

If you have outstanding or delinquent loans in the past that affects your status as a member and your capacity to apply for a loan, the Conso-Loan is a consolidation of five different loan products into one—Salary Loan, Restructured Salary Loan, Enhanced Salary Loan, Emergency Loan Assistance, and Summer One-Month Salary Loan that automatically fully settle your obligations from these loans.

What is the difference between a regular loan and a Conso-Loan?

A Regular loan is acquired for paying any kind of transaction a borrower needs it fit, may it be for personal consumption or any other transaction outside the GSIS. A Conso-Loan will be specifically used for any previous borrowing such as those mentioned above to fix any negative effects on your borrowing capacity with a member government organization.

Who can avail of the GSIS Conso-Loan?

- Active members with no pending administrative or criminal case are qualified to apply for the loan, provided their agency remitted at least 3 correct monthly premium payments (both personal and government share) within the last 6 months prior to the filing of the application.

- Must not be on leave of absence without pay.

- Members’ net take-home pay should be sufficient to cover the regular monthly amortization.

- Members from suspended agencies are not qualified to avail of the Conso-Loan.

How can members apply for a Conso-Loan?

Members with a GSIS eCard Plus can apply for the Conso-Loan via the GSIS Wireless Automated Processing System or G-W@PS kiosk placed in all GSIS servicing offices and select government agencies. Those still using the old eCard can apply for the loan, over-the-counter, in their servicing GSIS offices.

To apply for a Conso-Loan loan using the kiosk, members need to first place their eCard Plus on the card reader of the kiosk, then, they need to place any of their pre-selected fingers on the fingerprint biometric scanner of the kiosk. Using the touch screen monitor of the G-W@PS, members must select “Consolidated Loan” from the list of loans available on the loan menu and follow the simple instructions that will be displayed on the screen to complete the transaction. Then you will be updated if your loan has been granted or not.

GSIS eCard Plus

GSIS has made availing of their services easy and accessible for their members by introducing the GSIS eCard Plus. It serve as an Identification card that GSIS members can use as a disbursement card, ATM Card, VISA debit card, hospitalization discount card, medicine discount card, and tuition discount card to name a few.

How to enroll for an eCard Plus

- Bring two valid IDs (examples: company ID, LTO license, PRC license, passport, voter’s registration ID) to the nearest GSIS office nearest you

- Accomplish an eCard enrollment form and submit it to the GSIS personnel assigned in the eCard enrollment area

- In a few weeks, you can either get your eCard from the GSIS office where you applied or through snail mail

For PENSIONERS ABROAD, here are the steps on how to enroll for your eCard:

Through the use of Skype, a web-based software that allows users to make telephone calls over the Internet free of charge, pensioners abroad can enroll in the eCard.

To enroll in the eCard using Skype as a pensioner, you must have the following:

- a personal computer (either desktop or laptop),

- a webcam, headset with microphone or PC speakers

- a separate PC microphone, broadband internet connection

- a well-lit and quiet area where the PC is placed

- a passport and two more valid IDs

Any further inquiries about GSIS

The Social Security System (SSS)

About SSS

The “Paseguruhan ng Kapanatagang Panlipunan” or Social Security System (SSS) which began in 1957, is a social insurance program for workers in the Philippines. It is a government agency that provides retirement and health benefits to all enrolled employees in the Philippines. Members of the SSS can also make 'salary' or 'calamity' loans. Salary loans depend on the monthly salary of the employee. Calamity loans are for such times when there is a calamity that has been so declared by the government, in the area where the SSS member lives, such as flooding, earthquake and natural disasters.

Employees of the Philippine National Government do not contribute to SSS but rather have their own system, the Government Service Insurance System or GSIS.

Loans thru the SSS

Loans that can be availed are:

· Salary loans

· Pari-passu Housing Loan (partnership between SSS and affiliated partners)

· Housing Loan for Repairs and Improvement

· Corporate Housing Program

· Individual Housing

· Housing Development Loan

· Apartment and Dormitory

· Housing Loan for OFWs

· Housing Loan for Workers Organization Members

· Assumption of Mortgage

How to avail of these loans

ELIGIBILITY REQUIREMENTS

1. Only currently employed, currently contributing self-employed or voluntary member is qualified to avail of the program:

i. For a one-month loan, the member-borrower must have 36 posted monthly contributions, six (6) of which should be within the last 12 months

ii. Prior to the month of filing of application.

iii. For a two-month loan, the member-borrower must have 72 posted monthly contributions, six (6) of which should be within the last 12 months prior to the month of filing of application.

2. If the member-borrower is employed, his employer must be updated in contributions and loan remittances.

3. The member-borrower must be updated in the payment of his obligations in his member loans, which include salary, calamity, emergency, educational, stock investment, Member Assistance for the Development of Entrepreneurship (MADE) and housing loans granted under the Unified Housing Loan

Program (UHLP) or direct from SSS.

4. The member-borrower has not been granted final benefit, i.e., total permanent disability, retirement and death.

5. The member-borrower must be under sixty-five (65) years of age at the time of application (SSC Res. No. 434 dated 09 November 2005)

6. The member-borrower has not been disqualified due to fraud committed against the SSS.

Any further inquiries about SSS?

Are you a Foreigner in the Philippines?

Click here for you options