What will be discussed:

Who needs to File Income Tax Return?

Who are not required to file Income Tax Returns?

Who are exempt from Income Tax?

BIR Forms and Documentary Requirements

Steps and procedures for filing income tax return

Penalties for Late or Non-Filing of Income Tax

How to compute for your Income Tax

Every year, especially during April, most people are getting ready to file for their income tax returns. The Bureau of Internal Revenue (BIR) gives an ample amount of time for tax payers to prepare and file. Even on the local television or radio, there are announcements reminding not to rush until the last day as it might be crowded and if you don’t make it on time, there are additional penalties.

But what is an Income tax?

An income tax is a tax imposed by the government on the financial income of people or companies within their jurisdiction. By law, businesses and individuals must file an income tax return every year to determine whether they owe taxes or are eligible for a tax refund. Income tax is a key source of funds the government uses to fund its activities and for public service.

Who needs to file Income Tax Return?

A. Individuals

1. Resident citizens receivingincome from sources within or outside the Philippines

- Employees deriving income from 2 or more employers, concurrently or successively at any time during the taxable year

- Employees income regardless of the amount, whether from a single or several employers during the calendar year, the income tax of which has not been withheld correctly (i.e. tax due is not equal to the tax withheld) resulting to collectible or refundable return

- Self-employed individuals receiving income from the conduct of trade or business and/or practice of profession

- Individuals deriving mixed income, i.e., compensation income and income from the conduct of trade or business and/or practice of profession

- Individuals deriving other non-business, non-professional related income in addition to compensation income not otherwise subject to a final tax

- Individuals receiving income from a single employer, although the income of which has been correctly withheld, but whose spouse is not entitled to substituted filing

- Marginal income earners

2. Non-resident citizens receiving income from sources within the Philippines

3. Aliens, whether resident or not, receiving income from sources within the Philippines

B. Corporations no matter how created or organized including partnerships:

- Domestic corporations receiving income from sources within and outside the Philippines

- Foreign corporations receiving income from sources within the Philippines

- Taxable partnerships

C. Estates and trusts engaged in trade or business

Who are not required to file Income Tax Returns?

The following individuals are not required to file income tax returns:

1. An individual who is a minimum wage earner

2. An individual whose gross income does not exceed his total personal and additional exemptions

3. An individual whose compensation income derived from one employer does not exceed P60,000 and the income tax which has done correctly withheld.

4. An individual whose income has been subjected to final withholding tax (foreign employee as well as Filipino employee occupying the same position as that of the foreign employee or regional headquarter and regional operating headquarters of multinational companies, petroleum service contractors and sub-contractors and offshore-banking units, non-resident aliens not engaged in trade or business

5. Those who are qualified under “substituted filing”. However substituted filing applies only if all the following requirement are present:

- the employee received purely compensation income (regardless of amount) during the taxable year

- the employee received the income from only one employer in the Philippines during the taxable year

- the amount of tax due from the employee at the end of the year equals the amount of tax withheld by the employer

- the employee’s spouse also complies with all 3 conditions stated above

- the employer files the annual information return (BIR Form No. 1604-CF)

- the employer issues BIR Form No. 2316 (Oct 2002 ENCS version ) to each employee.

Who are exempt from Income Tax?

The following individuals are exempt from income tax:

1. A Non-resident citizen who is:

- A citizen of the Philippines who is physically present abroad with a definite intention to reside outside the Philippines

- A citizen of the Philippines who leaves the Philippines during the taxable year to reside abroad, either as an immigrant or for employment on a permanent basis

- A citizen of the Philippines who works and derives income from abroad and whoseemployment requires him to be physically present abroad most of the time during the taxable year

- A citizen who has been previously considered as a non-resident citizen and who arrives in the Philippines at any time during theyear to reside permanently in the Philippines will likewise be treated as a non-resident citizen during the taxable year in which he arrives in the Philippines, with respect to his income derived from sources abroad until the date of his arrival in the Philippines.

2.Overseas FilipinoWorker, including overseas seamen

An individual citizen of the Philippines who is working and deriving income from abroad as an overseas Filipino worker is taxable only on income from sources within the Philippines; provided, that a seaman who is a citizen of the Philippines and who receives compensation for services rendered abroad as a member of the complement of a vessel engaged exclusively in international trade will be treated as an overseas Filipino worker.

BIR Forms and Documentary Requirements

The following are the BIR Forms to be used for filing annual income tax return for different types of taxpayers.

1. BIR Form 1700

Annual Income Tax Return (For Individual Earning Purely Compensation Income Including Non-Business/Non-Profession Related Income)

Documentary Requirements:

- Certificate of Income Tax Withheld on Compensation (BIR Form 2316)

- Waiver of the Husband’s right to claim additional exemption, if applicable

- Duly approved Tax Debit Memo, if applicable

- Proof of Foreign Tax Credits, if applicable

- Income Tax Return previously filed and proof of payment, if filing an amended return for the same taxable year

2. BIR Form 1701

Annual Income Tax Return (For Self-Employed Individuals, Estates and Trusts Including Those With Both Business and Compensation Income).

Documentary Requirements:

- Certificate of Income Tax Withheld on Compensation (BIR Form 2316), if applicable

- Certificate of Income Payments not Subjected to Withholding Tax (BIR Form 2304) if applicable

- Certificate of Creditable Tax Withheld at Source (BIR Form 2307), if applicable

- Waiver of the Husband’s right to claim additional exemption, if applicable

- Duly approved Tax Debit Memo, if applicable

- Proof of Foreign Tax Credits, if applicable

- Income Tax Return previously filed and proof of payment, if filing an amended return for the same year

- Account Information Form (BIR Form 1701 AIF) or the Certificate of the independent CPA with Audited Financial Statements if the gross quarterly sales, earnings, receipts or output exceed P 150,000.00

- Proof of prior year’s excess tax credits, if applicable

3. BIR Form 1702

Annual Income Tax Return (For Corporations and Partnerships)

Documentary Requirements:

- Certificate of Income Payments not Subjected to Withholding Tax (BIR Form 2304), if applicable

- Certificate of Creditable Tax Withheld at Source (BIR Form 2307), if applicable

- Duly approved Tax Debit Memo, if applicable

- Proof of Foreign Tax Credits, if applicable

- Income tax return previously filed and proof of payment, if amended return is filed for the same taxable year

- Account Information Form (BIR Form 1702 AIF) and/or the Certificate of the independent CPA with Audited Financial Statements, if the gross quarterly sales, earnings, receipts or output exceed P150,000.00

- Proof of prior year’s excess tax credits, if applicable

Steps and procedures for filing income tax return

1. Fill-up corresponding BIR Form (BIR Form 1700, 1701 or 1702) in triplicate (3 copies)

2. Attach the corresponding documentary requirements

3. If there is payment:

· Proceed to the nearest Authorized Agent Bank (AAB) of the Revenue District Office where you are registered and present the duly accomplished BIR Form (return), together with the required attachments and your payment.

- In places where there are no AABs, proceed to the Revenue Collection Officer or duly Authorized City or Municipal Treasurer located within the Revenue District Office where you are registered and present the duly accomplished BIR Form, together with the required attachments and your payment.

- Receive your copy of the duly stamped and validated form from the teller of the AABs/Revenue Collection Officer/duly Authorized City or Municipal Treasurer.

4. For “No Payment” Returns including refundable returns, and for tax returns qualified for second installment:

- Proceed to the Revenue District Office where you are registered or to any Tax Filing Center established by the BIR and present the duly accomplished BIR Form, together with the required attachments.

- Receive your copy of the duly stamped and validated form from the RDO/Tax Filing Center representative.

Penalties for Late or Non-Filing of Income Tax

Every individual or entity required to file his/its income tax return and pay his/its corresponding income tax due is expected to beat thedeadline to avoid being penalized and imposed with additional charges such as 25% or 50% surcharge, 20% interest per annum and compromise penalty for non-filing and/or non-payment of taxes.

How to compute for your Income Tax

What you need to know :

Basic Salary : Php 15,000

Status : Single without dependent

Overtime Pay : Php 2.500

Late Deduction : Php500

Philhealth Contribution : Php 250

Pag-IBIG Contribution : 100

How to compute :

Taxable income = Monthly Basic Pay + Overtime Pay + Holiday Pay + Night Differential - Late Deduction - Absences - SSS/Pag-IBIG/Philhealth

Php 16,150 = 15,000 + 2,500 - 500 - 500 - 250 - 100

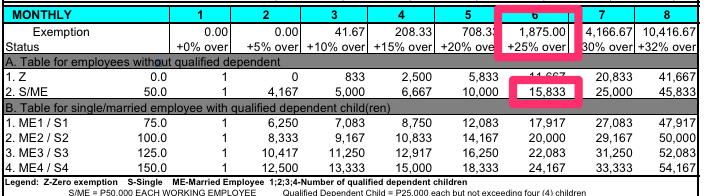

Your tax for the month is Php 1,954.25 (as per the BIR Tax Table at ftp://ftp.bir.gov.ph/webadmin1/pdf/42126AnnexC.pdf

Under S/ME look of the nearest figures with your taxable income and the nearest amount is 15,833 and the tax is Php 1,875.00 + 25% in excess of 15,833

So your tax is 15,833.00 = 1,875.00

Excess (16,150-15,833) = 317 X 25% = 79.25

Tax is ( 1,875.00 + 79.25)= Php 1954.25

Is there anything we missed?